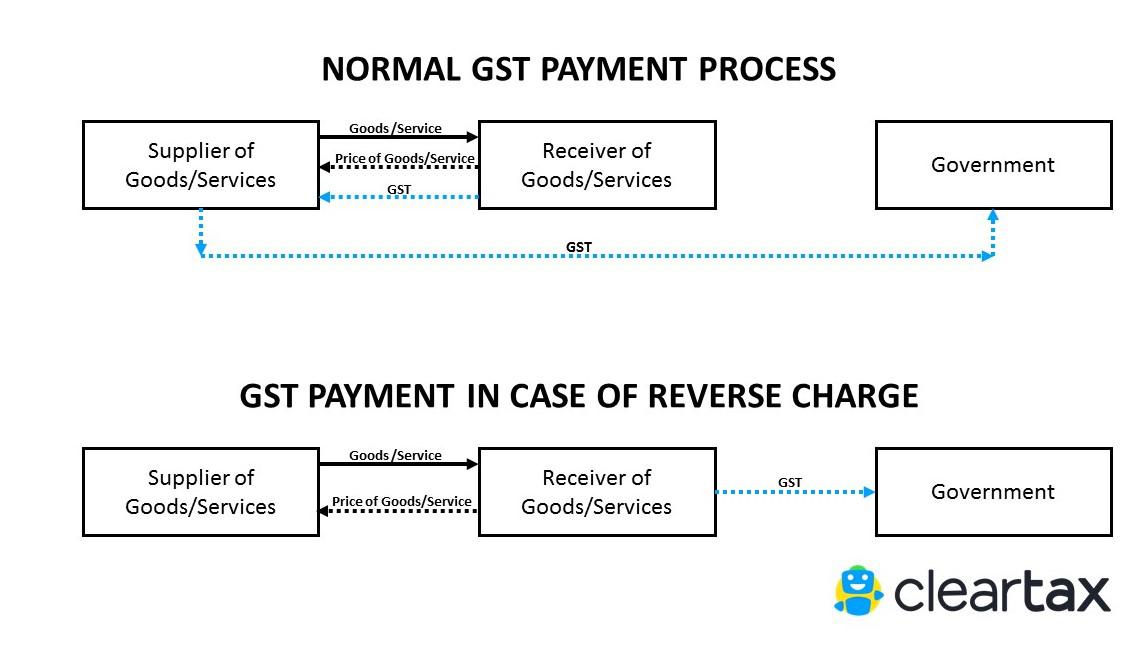

1. What is Reverse Charge?

Normally, the supplier of goods or services pays the tax on supply. In the case of Reverse Charge, the receiver becomes liable to pay the tax, i.e., the chargeability gets reversed.

2. When is Reverse Charge Applicable?

A. Supply from an Unregistered dealer to a Registered dealer

If a vendor who is not registered under GST, supplies goods to a person who is registered under GST, then Reverse Charge would apply. This means that the GST will have to be paid directly by the receiver to the Government instead of the supplier.

The registered dealer who has to pay GST under reverse charge has to do self-invoicing for the purchases made.

For Inter-state purchases the buyer has to pay IGST. For Intra-state purchased CGST and SGST has to be paid under RCM by the purchaser.

B. Services through an e-commerce operator

If an e-commerce operator supplies services then reverse charge will be applicable to the e-commerce operator. He will be liable to pay GST.

For example, UrbanClap provides services of plumbers, electricians, teachers, beauticians etc. UrbanClap is liable to pay GST and collect it from the customers instead of the registered service providers.

If the e-commerce operator does not have a physical presence in the taxable territory, then a person representing such electronic commerce operator for any purpose will be liable to pay tax. If there is no representative, the operator will appoint a representative who will be held liable to pay GST.

C. Supply of certain goods and services specified by CBEC

CBEC has issued a list of goods and a list of services on which reverse charge is applicable.

3. Time of Supply under Reverse Charge

A. Time Of Supply in case of Goods

In case of reverse charge, the time of supply shall be the earliest of the following dates:

- the date of receipt of goods

- the date of payment*

- the date immediately after 30 days from the date of issue of an invoice by the supplier

If it is not possible to determine the time of supply, the time of supply shall be the date of entry in the books of account of the recipient.

*This point is no more applicable based this Notification No. 66/2017 – Central Tax issued on 15.11.2017

Illustration:

- Date of receipt of goods 15th May 2018

- Date of invoice 1st June 2018

- Date of entry in books of receiver 18th May 2018

The Time of supply of service, in this case, will be 15th May 2018

B. Time Of Supply in case of Services

In case of reverse charge, the time of supply shall be the earliest of the following dates:

- The date of payment

- The date immediately after 60 days from the date of issue of invoice by the supplier

If it is not possible to determine the time of supply, the time of supply shall be the date of entry in the books of account of the recipient.

Illustration:

- Date of payment 15th July 2018

- Date immediately after 60 days from the date of issue of invoice (Suppose the date of invoice is 15th May 2018, then 60 days from this date will be 14th July 2018)

- Date of entry in books of receiver 18th July 2018

The Time of supply of service, in this case, will be 14th July 2018

4. What is Self Invoicing?

Self-invoicing is to be done when you have purchased from an unregistered supplier AND such purchase of goods or services falls under reverse charge.

This is due to the fact that your supplier cannot issue a GST-compliant invoice to you, and thus you become liable to pay taxes on their behalf. Hence, self-invoicing, in this case, becomes necessary.

To create such an invoices on ClearTax GST software, follow the below steps:

Step 1 – Click on ‘+ New Purchase Invoice’ to create a new invoice

Step 2 – As you can see, you need to fill data in multiple fields. Let’s understand each field in detail:

1. Enter the serial number of the bill into the field marked ‘Invoice Serial Number’. Since your supplier has not issued an invoice and you are creating an invoice on their behalf, you need to add a serial number on your own. You can create and maintain a serial number series for reverse charge bills, for easier invoicing

2. Enter the ‘Invoice Date’. This date must be based on time of supply

3. Enter any detail such as the order number etc., into the field marked ‘Reference Number’

4. Under ‘Due Date’, you have to mention the date by when you have to make the payment to the supplier for the purchase you made (mentioning this date is not mandatory)

5. Under ‘Vendor Name’, enter the supplier’s name. Remember this name cannot be your own name, even if you are doing self-invoicing under reverse charge

6. In case the vendor’s name is not set already, you can add a new vendor

7. Enter details of goods/ services purchased

8. From the drop-down under ‘Advance Settings’, select ‘Reverse Charge’

9. Now, fill in all the details displayed on your screen.

Step 3 – After filling all the other details, click on Save.

For more details

www.cleartax.in

It is really nice post. thank for sharing with us. it is very helpful for all people.

ReplyDelete